Global LED Video Display Sales Up 12.8% In Q1; Absen #1 Manufacturer, But Samsung, LG Catching Up

June 7, 2023 by Dave Haynes

LED video display shipments recovered globally by 12.8% YoY in the first quarter of 2023, according to a summary from the research firm Omdia. The recovery was seen in most regions, except for Japan and Western Europe.

Researcher Tay Taehoon Kim posted on Linkedin some of the highlights of a paywalled report – LED Video Displays Intelligence Service.

Despite inflation and global issues such as housing and energy cost increases affecting the ProAV market, LED video display sales results in 1Q23 were better than other display technologies (LCD and OLED), with increased demand from segmented verticals, including retail, stage displays, and virtual reality (VR) stages for filmmaking.

Applying virtual production (VP) systems, instead of green walls, for making films and TV programs became common worldwide, but not from China owing to relatively cheap labor costs so far. However, as labor and production costs also gradually increased in China, Chinese filmmakers also began to use VP with LED video displays to reduce production time and drive down costs. Because China’s cinema market is expected to recover after its economy reopens, the demand for LED video displays for VP will also increase.

In line with the growing demand for VP targeting LED video displays, many vendors are launching products for VP usage. Leyard announced plans to launch the Direct Light Pro series at InfoComm 2023. Also, LG Electronics launched LBAF, a new Magnit product equipped with technologies optimized for virtual production.

One of the interesting aspects of the current market is how demand is rising for premium displays and compelling manufacturers to develop and sell sub-1mm LED display products.

Because the impacts of inflation are expected to be less severe in 2023 than previously forecast, demand for relatively inexpensive wide pixel pitch products has returned to FPP products. In fact, the sales volume of FPP products (pixel pitch under 2mm) reached 15.5% YoY, surpassing the overall YoY growth of 12.8% for LED video display shipments. Because the demand for FPP products increases again, the competition between vendors to develop and sell top-spec products is heating up again. After Samsung launched its IWB product with 0.63mm pixel pitch, the company achieved its first sales in 1Q23. In May 2023, Unilumin officially launched UMicro 0.4, the finest pixel pitch product applying COB flip chip technology with a high contrast ratio and energy-saving technology.

Omdia believes this will drive down the ASP and cost for overall FPP products, especially for sub-1mm (including 0.8mm and 0.9mm) pixel pitch products.

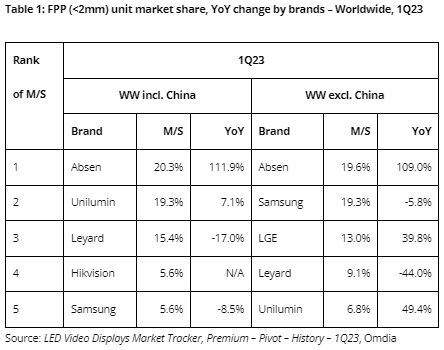

The summary also includes a chart that shows Absen is the biggest LED display manufacturer both in China and globally. The Chinese firm had a huge Q1 with triple-digit growth in market share. It’s notable that both Samsung and LG, who were barely in the LED display business a few years ago (especially LG), are now numbers two and three on the global market share chart. That would seem to speak to the power of having known and trusted brands, as well as much more extensive and established direct sales and channel capabilities.

Leave a comment