Public Information Display Market Up Almost 14% Year On Year: Omdia

December 11, 2023 by Dave Haynes

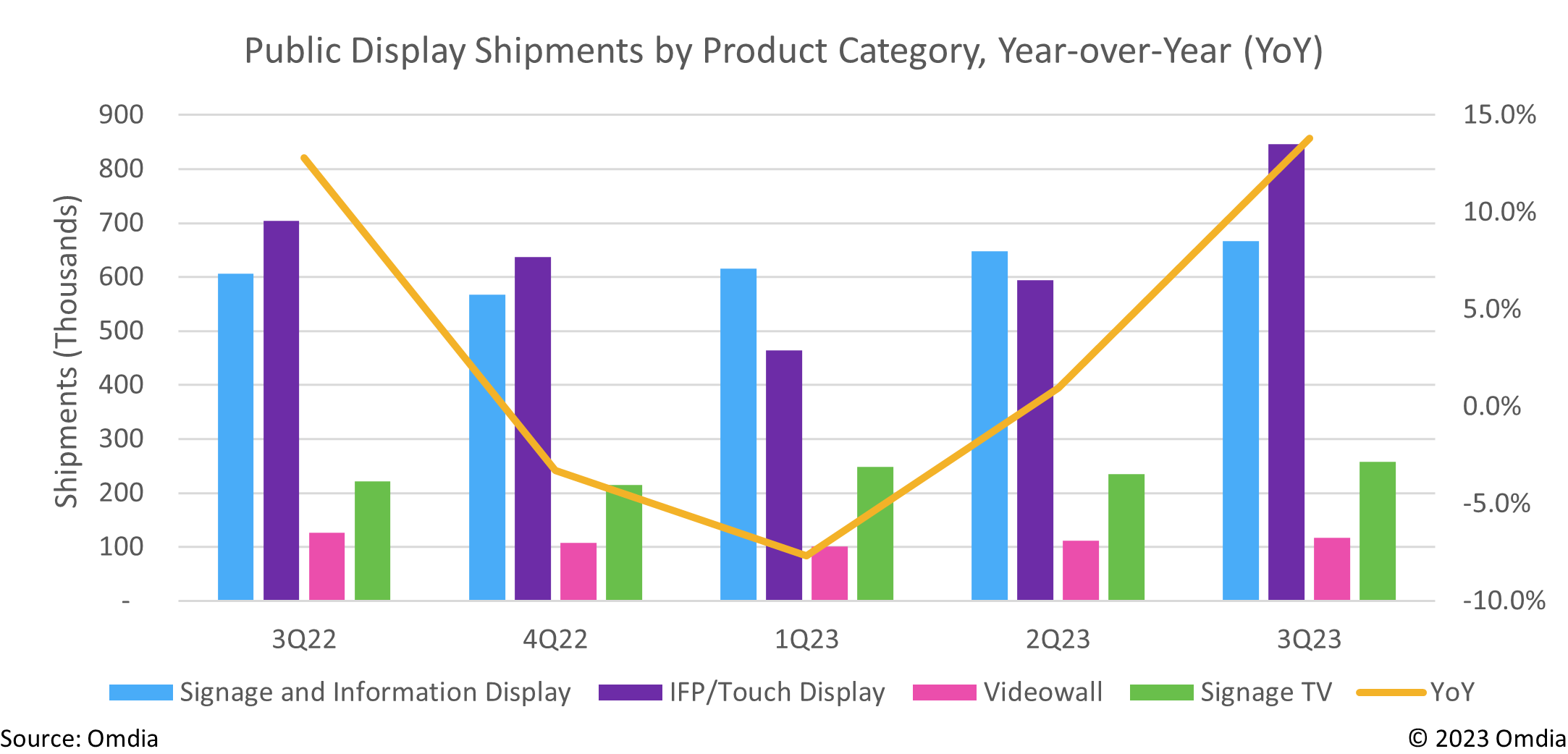

New research released by Omdia suggests the public information display market has bounced back from a dip a year ago, with interactive displays being the biggest growth driver in sales and shipments.

The research firm Omdia says in highlights from its fee-based Public Display Market Tracker 3Q23 that the public display market saw a 13.8% growth year-over-year (YoY) rise across multiple regions, with shipments of Interactive Flat Panel (IFP)/touch displays up 20.1% YoY, led by big growth in China.

“The increase in shipments for IFP/touch displays in China came from seasonal replacements of interactive displays in the education sector, primarily in the K-12 market. Majority of the IFP/touch display shipments were for 75-inch and 86-inch displays, comprising over 80% of China’s interactive displays this quarter,” says David Chai, Research Analyst at Omdia.

IFP/touch display performance in other key countries such as Turkey and Egypt also contributed to the particularly strong YoY results seen in both Eastern Europe and the Middle East & Africa, respectively.

Global signage and information shipments continue to demonstrate steady growth, although at a smaller rate of 2.8% quarter-over-quarter (QoQ). “Many projects are continuing to face extended timelines or postponement given the continued uncertainty in the global economy this year – especially within the corporate sector, as well as inflation concerns impacting major regions,” states Kelly Lum, Principal Research Analyst at Omdia.

Western Europe remains the leading region in this product category, albeit reporting flat QoQ performance for 3Q23 due to constrained economic conditions in key countries. North America ranks second in overall signage and information display shipments with a lift of 8.3% QoQ for 3Q23, experiencing milder impacts from inflation than Western Europe. “The beginning of 2023 in North America, especially in the US market, started off slow with concerns over economic health and layoffs affecting investments in the corporate sector, but we’ve started to see more traction now in the second half of 2023 as projects are progressing,” comments Lum.

105” 5K 21:9 displays make their debut from mainstream signage brands targeted for the corporate sector

Vendors such as Jupiter and Avocor were among the first brands to launch the 105” 5K displays with 21:9 ultra-wide aspect ratio, specifically targeted for hybrid meetings utilizing Microsoft Teams’ MTR Front Row feature. Many mainstream LCD vendors showcased similar products at Integrated Systems Europe (ISE) and InfoComm earlier this year, with noticeable interest in this product’s potential, but actual demand has yet to be seen.

Based on third quarter shipment results, vendors such as Hisense, Iiyama, Planar, and Viewsonic, started shipping these displays with nearly 500 units sold globally for both IFP/touch and non-touch models. Initial results show that over 65% of these displays sold within Western Europe and the Middle East, followed by Asia & Oceania at over 20% penetration.

While the 105” 21:9 display is still a niche market, the corporate sector is poised for growth with continued investment in meeting and boardroom upgrades in 2024. The additional display area that 21:9 offers over the traditional 16:9 format may also offer opportunities for expansion in other sectors as well, such as education settings or training facilities. These ultra-wide displays may also experience a further uptick in growth once Microsoft supports native 5K resolution instead of upscaling.

Chinese brands record strong shipment performance from domestic demand

Both SeeWo and Hitevision report significant growth for third quarter results as China’s economy is recovering from the downturn seen in 2022 from COVID impacts. SeeWo and Hitevision’s growth mainly stem from strong IFP/touch shipments within the K-12 and higher education sector, as replacement demand for these displays is fulfilled. Dahua, Goodview, Hisense, and MAXHUB remain among the leading brands in the region.

For 3Q23, China claims the largest regional share of public display shipments globally, comprising 34.8% share this quarter. North America and Western Europe rank second and third, with 20.6% and 17.8% share for 3Q23, respectively.

Long-term slowdown expected amid persistent uncertainties

Despite an encouraging 3Q23 performance in the public display landscape, a slowdown is anticipated heading into 2024 due to prolonged uncertainties. Key regions across the globe are expected to endure contrasting economic circumstances with inflation still a pressing issue and potential recession also on the cards.

According to Omdia’s Public Display Market Tracker 3Q23, China’s public display market has shown some positive momentum attributed to education sector-related activities. Additionally, consumer spending increased in 3Q23 owing to the tourism sector during the National Day Golden Week holiday. However, this growth may not be sustainable as the region is still marred by several economic issues including its property sector crisis.

There is also an upbeat sentiment in North America as consumer spending experienced an upsurge. While this indicates a resilient economy thus far, recession remains a possibility in North America.

Over in Asia & Oceania, India is expected to experience a strong growth trend well into 2024 owing to increased foreign investments, consumer purchasing power, and large-scale domestic activities across all sectors.

Leave a comment